What the Data Actually Shows

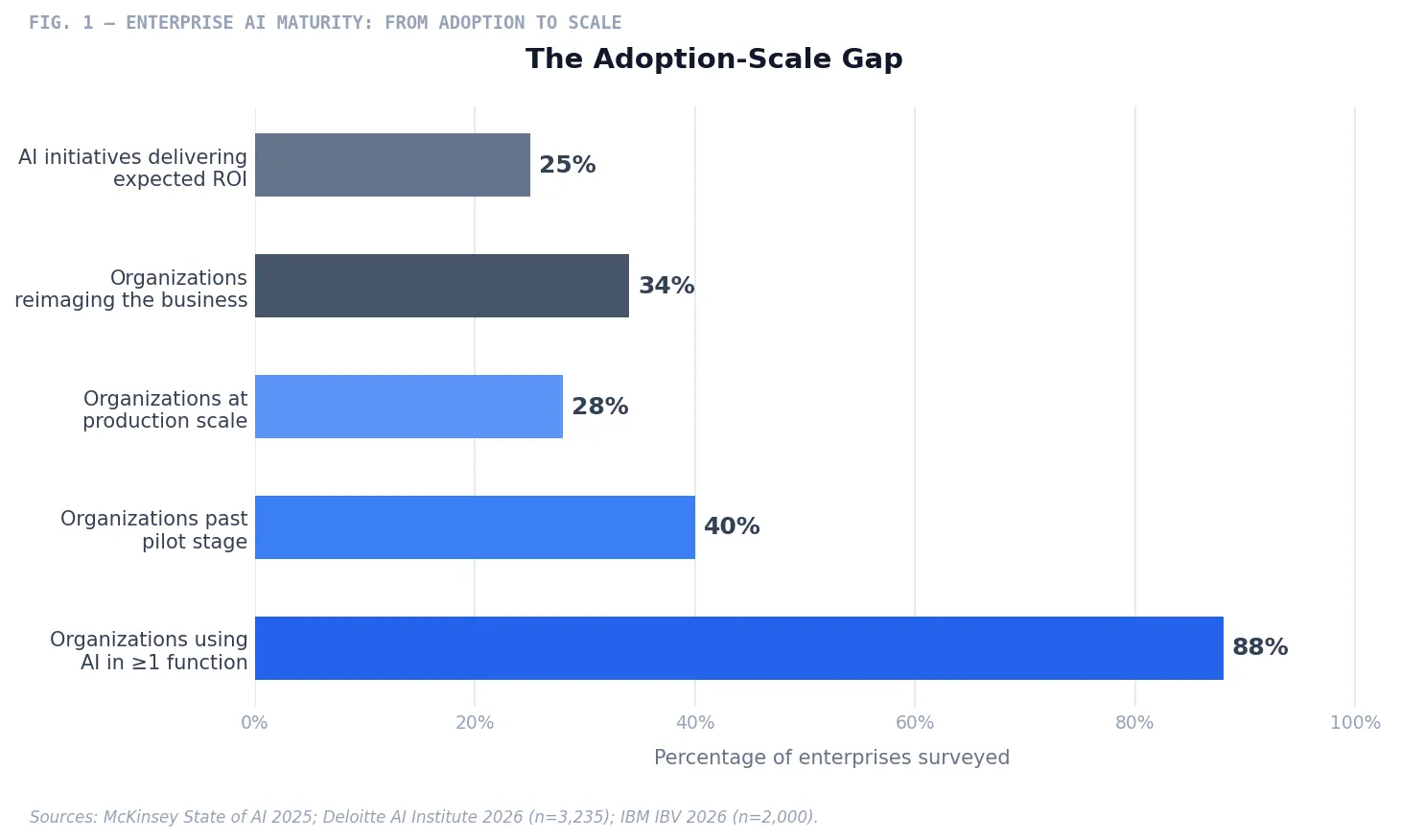

In the spring of 2026, IBM’s Institute for Business Value published findings from a survey of two thousand CEOs across thirty-three countries. Ninety-seven percent reported that their organizations were benefiting from AI.1 Only twenty-nine percent reported significant organizational ROI.2

That gap is not a failure signal—it is a maturity signal. Most large organizations are somewhere in the middle of a normal technology adoption curve, past the point of asking whether AI creates value and now grappling with the harder question of how to make that value consistent and compound.

Deloitte’s AI Institute, drawing on 3,235 senior leaders across twenty-four countries, found that sixty-six percent of organizations report productivity and efficiency gains, twenty percent are already growing revenue through AI initiatives, and thirty-four percent are actively reimagining core business processes rather than simply augmenting existing ones.3 McKinsey’s numbers tell a similar story from a different angle: eighty-eight percent of organizations have AI running somewhere in the business, forty percent have moved past pilot, and twenty-eight percent have reached genuine production scale across multiple functions with outcomes they can measure.4

Gartner projects global AI spending at $2.5 trillion in 2026.5 Average enterprise AI budgets are tracking toward $11.6 million—up sixty-five percent from 2025.6 Capital is not the bottleneck. The organizations reaching production scale are distinguished not by how much they spent, but by the organizational conditions they built before they spent it.

The Stanford Findings: What Works

In April 2026, Stanford’s Digital Economy Lab published a study of fifty-one successful AI deployments across forty-one organizations, nine industries, and seven countries. Every case was live in production, delivering measurable business value, and capable of further scaling.7 The research team—Erik Brynjolfsson, Elisa Pereira, and Alvin Wang Graylin—wanted to reverse-engineer what these organizations had in common, including the friction that did not make it into press releases.

What they found should reorient how enterprise leaders think about where the real implementation work lives.

“The central thesis is clear: AI success is not a technology problem. It is an organizational transformation problem.”

— Stanford Digital Economy Lab, The Enterprise AI Playbook, April 2026

Ninety-five percent of deployment shortfalls across the study traced back to organizational factors—workforce unpreparedness, missing governance, or absent executive ownership—rather than to model performance or integration complexity.8 The winning organizations were not running better models. They were running a better sequence: workflow mapping before technology selection, governance embedded from day one, observability established before production launch, and leadership continuity held through the first eighteen months regardless of early setbacks.9

One finding in particular stands out. All seven cases in the study that achieved organization-wide transformation had sponsors who treated AI adoption as a performance metric across the enterprise, not as a discrete project to support from a distance.10 That is a meaningful distinction. Sponsorship that shows up at kickoffs and quarterly reviews is different from sponsorship that changes how functions are evaluated.

The broader implication is worth sitting with. Organizational design, sequencing, and governance are within direct leadership control in ways that model capability is not. The organizations that have cracked production-scale deployment did so by solving a people and process problem, not a technology one.

Building a Governed AI Stack

The typical large enterprise in 2026 is not running one AI system. According to Larridin’s research, most organizations now operate multiple foundation model relationships simultaneously, alongside AI-first products, AI-augmented SaaS tools, and an expanding fleet of autonomous agents—many of them deployed by individual teams without central visibility.11 Enterprises with more than one thousand employees deploy an average of fourteen to eighteen distinct AI tools, a number that has roughly doubled since 2023.12

That proliferation is not inherently a problem. It becomes one when there is no inventory of what is running, no clear ownership of what each tool can access, and no procurement logic that asks whether a new tool duplicates something that already exists. Each custom API integration in that landscape costs an estimated $45,000–$120,000 to build and maintain over three years.13 A fourteen-tool footprint can carry $1.26M–$5.04M in integration debt that never appears on an AI budget line.

Cost Visibility The license fee is roughly 25% of true AI total cost of ownership. Integration, governance, training, and rework absorb the remaining 75%—categories that rarely appear in procurement proposals or board investment cases.

There is also a security dimension, though it is more tractable than it is often framed. When employees cannot find an approved tool that actually meets their needs, many route around IT entirely—Netskope’s 2026 data finds forty-seven percent of generative AI users access tools through personal accounts.14 Providing enterprise-grade alternatives that compete on capability and convenience, not just on policy compliance, reduces that rate by eighty-nine percent.15 The governed stack wins when it is also the better option.

Leading organizations are moving toward centralized AI platform functions that own the approved stack, enforce access through single sign-on, and require new tool adoption to justify itself against existing capabilities before approval. Thirty-nine percent of enterprise leaders report already attempting to reduce tool counts; forty-four percent have created formal AI usage policies.16 The organizations further along in this work have stopped treating governance as a control function and started treating it as an infrastructure function—the foundation on which everything else is built.

Building Workforce Capability at Scale

Skills are the biggest barrier to AI integration, full stop. Not infrastructure. Not budget. Not data readiness. Deloitte’s survey of 3,235 senior leaders puts workforce capability at the top of the list by a significant margin.17

Fifty-three percent of organizations are responding with broad AI fluency education. Forty-eight percent are running structured upskilling programs. Fewer than a third are redesigning career paths and job architectures to reflect how work is actually changing.18 All three matter—but they operate at different timescales and produce different outcomes, and the organizations conflating them tend to underinvest in the two that are harder.

Return Signal Organizations with mature workforce AI enablement programs achieve 3.8x higher returns on AI investments than those taking an ad-hoc approach, and deploy new AI capabilities 67% faster, according to enterprise learning research published in early 2026.

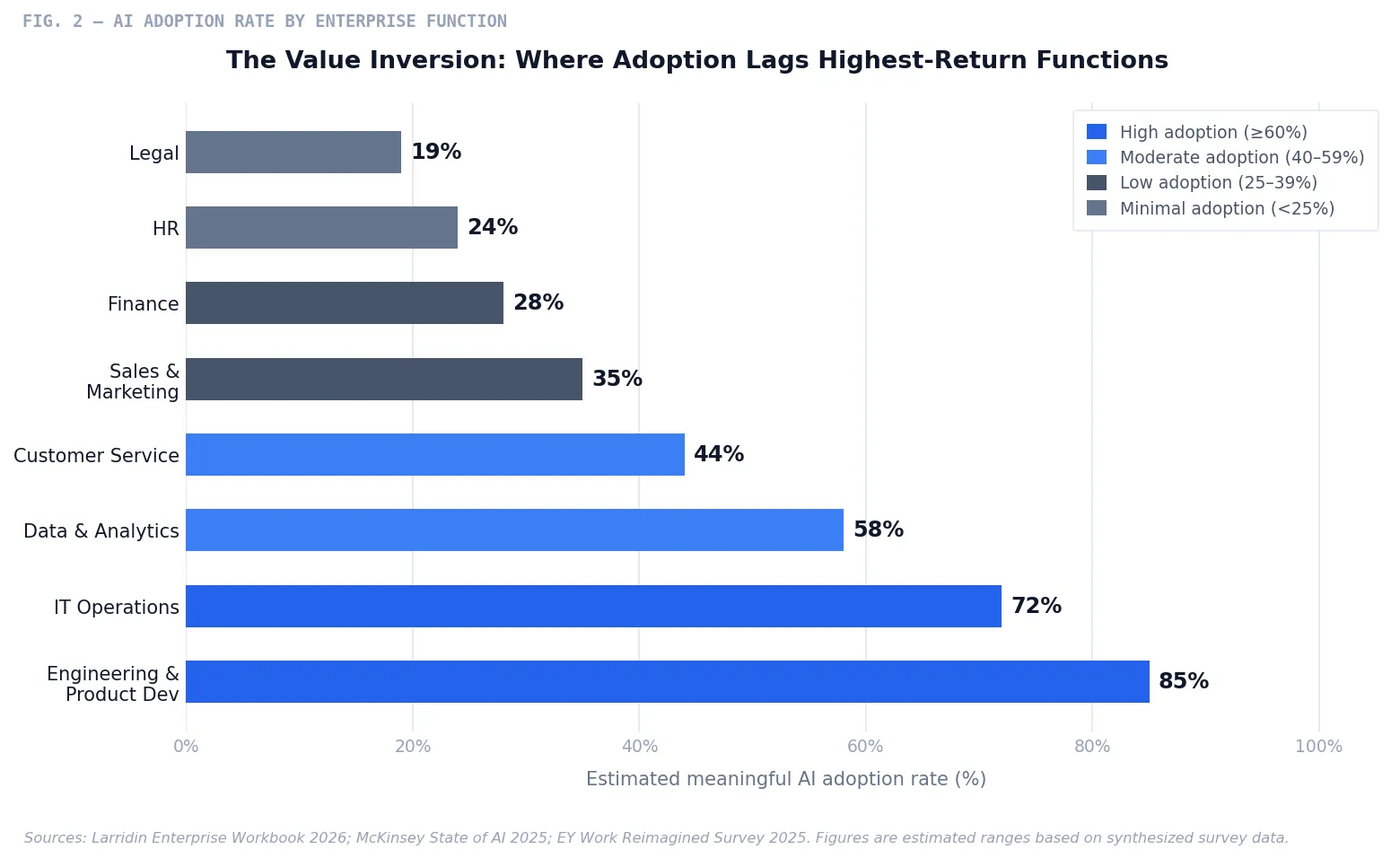

The adoption gap by function is the starkest illustration of where the opportunity sits. Engineering teams in mature organizations operate at 80–90% meaningful AI adoption. Most business functions—sales, finance, HR, legal—sit between 20% and 40%.19 Engineering got there first partly because the tooling matured first: coding assistants from GitHub, Cursor, Amazon, JetBrains, and others gave developers a well-worn on-ramp. Business functions are earlier in that curve, with a less developed tool ecosystem and less established practitioner culture around AI integration.

This creates an inversion worth paying attention to. McKinsey estimates that sales and marketing alone account for twenty-eight percent of the total economic potential of generative AI—more than any other function.20 The functions with the highest upside are among the least deployed. BCG’s 10-20-70 framework offers the structural explanation: ten percent of AI value comes from the model, twenty percent from the technology and data layer, and seventy percent from how people and processes are organized around both.21 You cannot close that gap with a license purchase.

Organizations allocating fifteen to twenty percent of total AI investment to workforce enablement consistently outperform those that minimize training spend.22 The format that produces the best outcomes is role-specific, applied to real work, and delivered in short increments rather than in intensive seminars. Programs that designate AI champions within each business function—people whose job it is to coach colleagues through actual use cases rather than abstract concepts—tend to accelerate adoption faster than any other single intervention.23

Modeling the Full Cost of AI Investment

Most enterprise AI budgets are modeled on the visible costs: licenses, compute, headcount. The costs that surface later—and often catch finance teams off guard—are the ones embedded in how AI actually operates inside a real organization.

McKinsey’s analysis of seventeen global companies found that AI now consumes up to a third of technology change budgets while simultaneously adding to run costs, since AI systems require ongoing model maintenance, platform governance, and control layers that do not replace legacy infrastructure—they layer on top of it.24 A majority of organizations underestimate AI costs by more than ten percent; nearly a quarter underestimate by fifty percent or more.25 KPMG’s Q4 2025 AI Pulse Survey puts average projected AI deployment spend at $124 million annually, with actual total cost of ownership running substantially higher once integration debt, governance overhead, and proficiency-related rework are included.26

That last category deserves specific attention. Workday’s January 2026 study found that thirty-seven percent of time nominally saved by AI is lost to rework in organizations where employees have not yet reached consistent proficiency.27 This is sometimes called the AI tax—the productivity drag that accumulates when rollout outpaces enablement. It is a real cost, but it is also a temporary one. IDC and Microsoft measure a 3.7x average return per dollar invested in generative AI across enterprises at production-scale deployment.28 That return is available; getting to it means building an accurate picture of total cost structure upfront rather than discovering it in year two.

Organizational Design for AI at Scale

The Chief AI Officer is now the fastest-growing executive title in the enterprise. IBM’s Institute for Business Value found that seventy-six percent of organizations have a CAIO in 2026, compared to twenty-six percent just one year prior.29 Among FTSE 100 companies, nearly half have appointed one, with sixty-five percent of those appointments made in the last two years.30

IBM’s research also found that organizations with a CAIO generate a five percent higher return on AI investments than those without one.31 That premium is consistent enough across the survey population to be structural rather than coincidental. The explanation, as IBM Research Director Jacob Dencik describes it, is that the role has evolved: early CAIOs were largely evangelists and internal advocates; the ones creating value now are operational drivers responsible for moving organizations from pilots into wide-scale production.32

The structural model that has shown the strongest results is hub-and-spoke rather than fully centralized. Schneider Electric’s approach—a central team that owns strategy, standards, and tooling, with execution embedded inside business units—is the architecture IBM’s 2026 research finds yields thirty-six percent higher ROI than decentralized alternatives.33 It keeps governance consistent while keeping AI close enough to real operational problems to actually get adopted.

The title alone, however, is not the answer. AVOA founder Tim Crawford draws the comparison to the CDO wave of the 2010s, where many organizations created the role before they had created the mandate.34 The CAIO moment has genuine structural logic behind it, but the value comes from budget authority, board-level access, and an organizational design that actually routes AI decisions through the role. Stanford’s Enterprise AI Playbook adds one more dimension: the organizations that achieved the widest transformation were not just the ones with a designated AI leader—they were the ones that made AI outcomes a performance expectation embedded across the entire enterprise, not something owned by a single function.35

Governance as Enabler, Not Constraint

The most useful frame for AI governance in 2026 is operational visibility rather than regulatory compliance. An organization that can inventory what AI systems are running, what data each one touches, and how decisions are being made is positioned to scale. One that cannot is not necessarily more exposed to risk—it simply has no way to assess what its exposure is.

Gravitee’s 2026 State of AI Agent Security Report surveyed over nine hundred executives and technical practitioners and found that eighty-one percent of technical teams have moved past planning into active testing or production for AI agents.36 Only fourteen percent report all agents going live with full security and IT approval.37 Read another way: the majority of organizations have agent deployments already underway and an opportunity to build formal governance around what is informally functioning today.

The regulatory environment is adding structure to that process whether organizations seek it or not. The EU AI Act’s high-risk obligations take effect in August 2026, covering an estimated forty-two percent of enterprise AI deployments—hiring tools, credit scoring systems, diagnostic applications, and others.38 Enterprise spending on AI governance tools reached $2.8 billion in 2025 and is projected to triple by 2028 per IDC.39 That trajectory reflects something real: organizations are building governance as infrastructure because the alternative is building it reactively, which costs more.

Governance Standard Treat each AI agent as a first-class security principal with its own identity, scoped permissions, and audit trail—not as an extension of an existing human user account or shared service credential. Agent identity management is the governance frontier most organizations have not yet reached, and the one with the widest current gap between deployment and control.

McKinsey’s research finds that sixty-five percent of AI high performers have defined human-in-the-loop processes to determine when model outputs need human review, versus twenty-three percent of other organizations.40 That gap—nearly three to one—correlates directly with sustained ROI. Governance done well is not a friction layer on top of AI deployment. It is the mechanism that makes sustained deployment possible.

The Platform Bet: Governance Over Model Leadership

The leading vendors in enterprise AI have largely converged on the same read of what enterprises need most right now, and it is not a better model. It is better governance infrastructure.

Microsoft’s Build 2026 announcements focused heavily on securing the development lifecycle—agent identity, policy-controlled deployment, access governance—through new capabilities in Agent 365 that let organizations inventory and govern agents across the stack.41 The broader logic is to embed governance into platforms enterprises already operate rather than requiring separate procurement. With ninety percent of Fortune 500 companies using Microsoft 365 Copilot in daily workflows and twenty-six million active GitHub Copilot users, the distribution advantage is real—observability and control can extend through existing contracts rather than new ones.42

The other major platforms are making similar bets, from different starting positions. Amazon Q Developer, Salesforce Einstein, ServiceNow, and Atlassian are each working toward deeper workflow integration and governance capability as the differentiating layer, not model performance. The model benchmarks change quarterly; the procurement relationship and the data integration depth are stickier. Eighty-one percent of enterprises now run three or more model families, up from sixty-eight percent a year ago.43 Model selection has become a portfolio decision, not a loyalty decision.

For enterprise buyers, the practical implication is to evaluate AI platforms on integration depth, governance capability, data residency controls, and auditability—not on the benchmark rankings published at the time of procurement. The rankings will shift. Those other dimensions are what determine whether investment compounds.

Six Decisions That Scale AI

The evidence across Stanford, McKinsey, Deloitte, IBM, and Gartner is consistent enough to distill into a practical set of decisions. These are not sequential steps so much as simultaneous structural commitments—organizations that get them right tend to get them right together.

1. Map workflows before selecting tools. The most common reason pilots fail to scale is that technology was selected before the underlying workflow was understood or redesigned. AI does not automatically improve a broken process. It often accelerates it. Organizations that map what they want to change—and redesign it first—have a dramatically clearer picture of what to buy and a much higher conversion rate from pilot to production.

2. Build a governed AI stack. There is a meaningful difference between a list of approved tools and an AI infrastructure the organization actually governs. The latter requires a continuous, auto-updating inventory of all AI tools, models, agents, and integrations; clear ownership for each; and a vetting process that requires new tool adoption to prove non-duplication before approval. The approved stack should also be the better option—employees who find workarounds do so because the sanctioned alternative was not good enough.

3. Fund training as infrastructure, not as an afterthought. Budget $2,000–$5,000 per employee for comprehensive AI upskilling, and allocate fifteen to twenty percent of total AI investment to workforce enablement.44 Build tiered, role-specific programs. Designate AI champions within each business function. The six-times productivity gap between AI super-users and average users working with the same tools is a proficiency gap—and it closes with deliberate investment, not with more licenses.45

4. Assign executive ownership with real authority. One executive needs to own AI strategy, governance, and ROI accountability with genuine budget authority and board-level visibility. A hub-and-spoke model—centralized strategy, standards and tooling; execution embedded within business units—consistently outperforms both extremes on return metrics. The title matters less than whether the organizational design actually routes AI decisions through the role or around it.

5. Treat agents as security principals. Each AI agent needs a distinct identity, scoped permissions, an audit trail, and defined procedures for access revocation. Full security and IT approval should be required before production deployment, with human-in-the-loop checkpoints calibrated to the risk level of what the agent can do. This is the governance frontier where most organizations currently have the widest gap between what is deployed and what is controlled.

6. Measure outcomes, not activity. Daily active users and prompt volumes tell you whether people are showing up. They do not tell you whether the business changed. Define the specific workflow-level outcomes that AI investment is expected to produce, establish baselines before deployment, and report against them. Sustained board confidence in AI investment follows from being able to answer one question: what is measurably different in this business because of this investment?

The Sequence Is the Strategy

Across fifty-one case studies, four major research bodies, and thousands of senior leader surveys, the evidence keeps landing in the same place: the organizations scaling AI successfully are doing so because they got the sequence right. Organizational readiness before tool selection. Governance embedded before production. Training resourced before broad rollout. Executive ownership established before the scale of the work made it essential.

None of those things require a breakthrough in model capability. They require decisions that leaders at the CAIO, CTO, and director of development level are already positioned to make—and the organizations that make them deliberately, rather than reactively, are the ones the data consistently shows compounding their early AI investments into durable competitive advantage.

References

- IBM Institute for Business Value, “The Rise and ROI of the Chief AI Officer,” IBM Think, June 2026.

- Writer and Workplace Intelligence, “Enterprise AI Adoption in the Enterprise 2026,” May 2026.

- Deloitte AI Institute, “State of AI in the Enterprise 2026,” survey of 3,235 senior leaders, August–September 2025.

- McKinsey & Company, “The State of AI: How Organizations Are Rewiring to Capture Value,” 2025.

- Gartner, “Gartner Says Worldwide AI Spending Will Total $2.5 Trillion in 2026,” press release, January 15, 2026.

- Multiple sources synthesized: a16z Growth Survey (January 2026); Larridin, “State of Enterprise AI 2026.”

- Elisa Pereira, Alvin Wang Graylin, and Erik Brynjolfsson, “The Enterprise AI Playbook: Lessons from 51 Successful Deployments,” Stanford Digital Economy Lab, April 2026.

- Ibid.

- Ibid.; summarized in “Stanford AI Playbook: Why 95% Fail Before Technology,” THE D[AI]LY BRIEF, April 2026.

- Pereira, Graylin, and Brynjolfsson, The Enterprise AI Playbook.

- Larridin, “AI Adoption: The Complete Enterprise Guide 2026,” May 2026.

- Worqlo, “Enterprise AI Tool Sprawl: What It’s Really Costing You,” May 2026.

- Ibid.

- Netskope, Cloud and Threat Report 2026.

- Healthcare Brew, “Shadow AI Governance in Healthcare,” 2026; cited in Vectra AI, “Shadow AI Explained,” May 2026.

- Zapier, “AI Sprawl Survey,” December 2025.

- Deloitte AI Institute, “State of AI in the Enterprise 2026.”

- Ibid.

- Larridin, “AI Adoption: The Complete Enterprise Workbook 2026,” March 2026.

- McKinsey & Company, “The Economic Potential of Generative AI,” 2023; referenced in 2025 State of AI update.

- BCG, 10-20-70 framework, widely cited; referenced in Larridin Enterprise Workbook 2026.

- Larridin, “AI Adoption: The Complete Enterprise Workbook 2026.”

- CCSLA Learning Academy, “How to Implement Enterprise AI Training Strategy in 2026,” March 2026; Udemy Business, “AI Upskilling Guide,” November 2025.

- McKinsey & Company and Serviceware, “Recalibrating CIO Technology Budgets for the AI Era,” March 2026.

- CIO.com, “How CIOs Can Get a Better Handle on Budgets as AI Spend Soars,” November 2025.

- KPMG, “Q4 2025 AI Pulse Survey”; cited in Larridin Enterprise Workbook 2026.

- Workday, workforce productivity study, January 2026; cited in Larridin Enterprise Workbook 2026.

- IDC and Microsoft, generative AI ROI measurement; cited in Paul Okhrem, “Enterprise AI Agents Adoption Statistics 2026,” June 2026.

- IBM Institute for Business Value, “The Rise and ROI of the Chief AI Officer,” IBM Think, June 2026.

- DataIQ, “2025 AI and Data Leadership Executive Benchmark Survey.”

- IBM Institute for Business Value, “The Rise and ROI of the Chief AI Officer.”

- Jacob Dencik, Research Director, IBM IBV, quoted in IBM Think, June 2026.

- IBM IBV, 2026 AI operating model research; cited in EdStellar, “4 Key Roles & Responsibilities of the Chief AI Officer,” December 2025.

- Tim Crawford, AVOA, quoted in IBM Think, “The Rise and ROI of the Chief AI Officer,” June 2026.

- Pereira, Graylin, and Brynjolfsson, The Enterprise AI Playbook.

- Gravitee, “State of AI Agent Security 2026 Report,” February 2026.

- Ibid.

- Gartner, cited in Medha Cloud, “60 Enterprise AI Statistics for 2026,” March 2026.

- IDC, enterprise AI governance spending projection; cited in Medha Cloud, “60 Enterprise AI Statistics for 2026.”

- McKinsey & Company, State of AI 2025; referenced in Pereira, Graylin, and Brynjolfsson, The Enterprise AI Playbook.

- Microsoft Security Blog, “Microsoft Build 2026: Securing Code, Agents, and Models Across the Development Lifecycle,” June 2026.

- Multiple sources: a16z Growth Survey, January 2026; Larridin, “AI Adoption: The Complete Enterprise Guide 2026.”

- a16z Growth Survey, January 2026; cited in multiple Q1 2026 enterprise AI summaries.

- Larridin, “AI Adoption: The Complete Enterprise Workbook 2026”; iternal.ai, “AI Training for Employees 2026.”

- OpenAI, State of Enterprise AI 2025, cited in Larridin Enterprise Workbook 2026.