When a Storage Bill Goes Viral, Pay Attention

On June 16, 2026, Hugging Face CTO Julien Chaumond posted a chart with no commentary other than the observation that Mistral had just uploaded a private model checkpoint to Hugging Face and, in doing so, drove total Hub storage from roughly 400 to nearly 1,200 petabytes in a matter of hours—an 800 PB single-event increase. His caption: “it broke our S3 bill.”1 Within hours, social media declared Hugging Face “bankrupt”—a dramatic overstatement, but one that exposed a genuine structural tension. A single model upload, from a single company, visibly strained the economics of one of the most well-funded AI infrastructure platforms in existence.

The “bankruptcy” framing was meme, not fact. But the underlying signal was real. At Amazon S3’s published list rate of roughly $23 per TB per month, an 800-petabyte storage event represents a theoretical one-month bill increment of approximately $18.4 million—before egress, request fees, or redundancy costs.2 Hugging Face absorbs substantial infrastructure cost as a public good. That public-good posture is only sustainable as long as investors remain willing to subsidize it. Which brings us to the actual story.

The Signal The Hugging Face story is not about one company’s bill. It is about what happens when the infrastructure costs of AI become too large to hide—and why enterprises building on AI platforms need to understand which vendors have real economics under the hood.

The Structural Unprofitability of Frontier AI

The most consequential financial fact in the enterprise technology market right now is one that rarely appears in procurement conversations: the companies whose models you are likely evaluating are, almost without exception, not profitable. The inference costs embedded in flat-rate subscriptions and generous free tiers are being underwritten by venture capital attracted to extreme paper valuations. The numbers are not ambiguous.

OpenAI’s 2025 operating loss of $20.9 billion was confirmed through financial documents reviewed by the Financial Times and reported broadly in June 2026.3 In the first quarter of 2026 alone, the company reported sales of $5.7 billion against an operating margin of negative 122 percent—an annualized loss trajectory approaching $28 billion.4 Internal documents shared with investors project that 2028 will see operating losses balloon to approximately three-quarters of that year’s revenue before any meaningful profitability arrives.5

xAI’s ratio is more alarming still: for every dollar it earns, it loses roughly $26.6

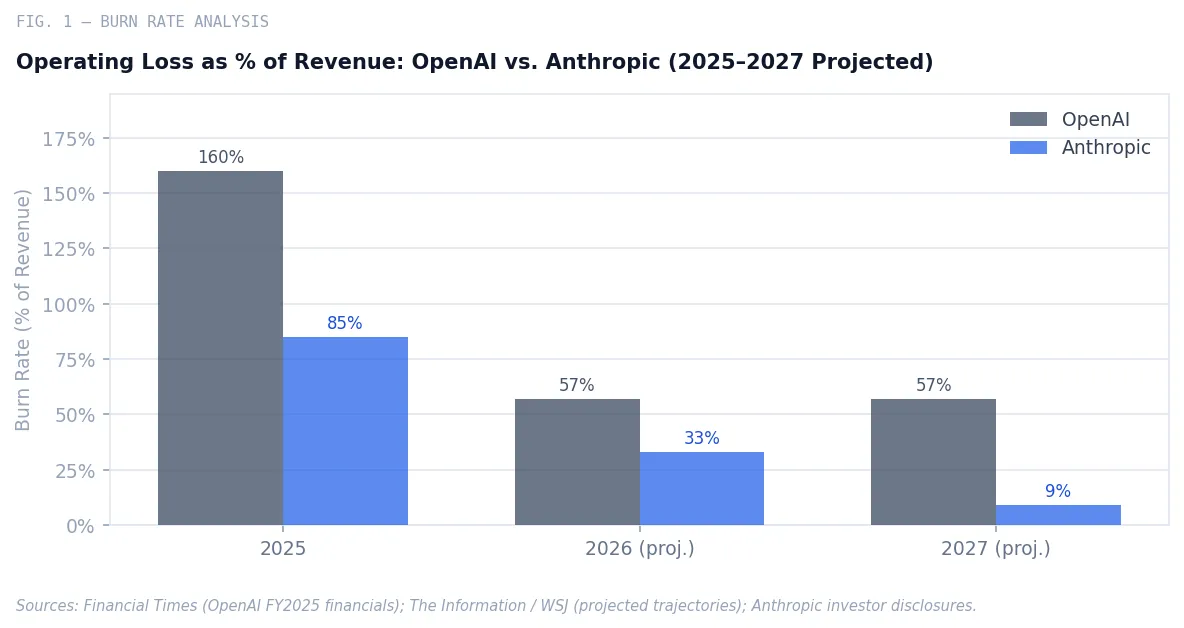

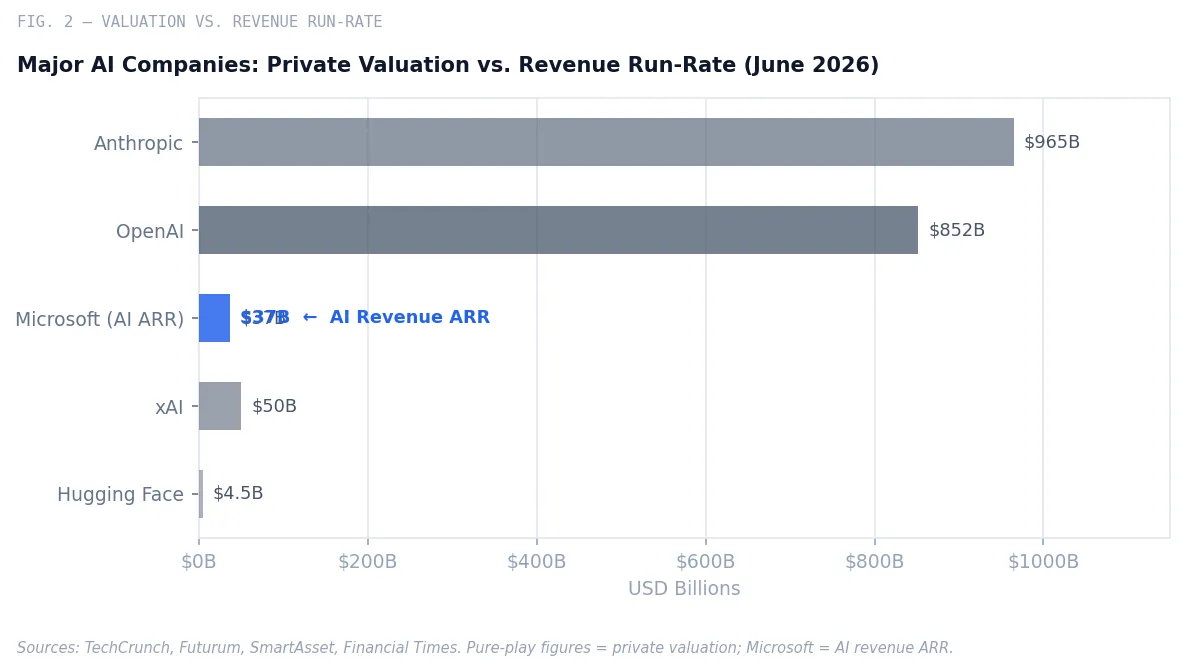

Anthropic’s trajectory is materially different—its burn rate is projected to fall to roughly 33 percent of revenue in 2026 and 9 percent by 2027, with cash-flow positivity expected by 2027 or 2028.7 Its annualized revenue run-rate crossed $47 billion in May 2026, having grown from $1 billion in December 2024.8 But its $965 billion private valuation—anchored by a $65 billion Series H closed May 28, 2026—is a multiple of roughly 20 times forward revenue on a company without disclosed sustained GAAP profitability.9 OpenAI’s $852 billion valuation trades at approximately 34 times forward revenue of $25 billion. These are not investment-grade multiples rooted in cash generation; they are bets on dominance underwritten by capital with more unrealized than realized value behind it.

The Mechanics of “Funny Money” AI Economics

Carta’s Q1 2026 fund performance report documents the mechanic clearly: unrealized valuations of VC-owned assets are rising, but realized gains remain rare. In the 2019 and 2020 fund vintages, median distributions-to-paid-in (DPI) ratios are barely above zero; less than half of all funds have returned any capital to their limited partners.10 Bain’s Private Equity Outlook 2026 estimates approximately 32,000 private companies representing $3.8 trillion in value remain unsold—most of that value existing only on paper until an exit event occurs.

“Venture funds can report attractive unrealized gains based on valuation marks, but limited partners ultimately receive returns only when companies exit and cash is distributed.”

— Qubit Capital / Bain Private Equity Outlook 2026

The implication for enterprise buyers is direct: favorable per-seat pricing, unlimited-query tiers, and heavily subsidized inference costs from pure-play AI vendors are not the product of efficient unit economics. They are investor capital transferred to customers as a customer-acquisition strategy—one that holds only as long as the next funding round arrives before the cash runs out.

This is not a novel dynamic. During the dot-com era, companies subsidized customer acquisition with investor capital until liquidity dried up and unit economics reasserted themselves. The AI era runs the same playbook at larger scale: AI startups captured 53 percent of global venture funding in the first half of 2025—$258.7 billion of $427.1 billion invested globally.11 That capital is, in material part, flowing to enterprise buyers as below-cost inference pricing.

When the exit environment tightens—when two-thirds of unicorn IPOs price below last private valuation, as they did through 2025—the funding arithmetic changes. Companies that cannot demonstrate credible unit economics will face the same choice Hugging Face faced with its S3 bill: absorb the cost, raise prices, or exit the market.

What This Means for Enterprise Buyers A procurement decision anchored to today’s subsidized pricing from a pure-play AI vendor is a bet that the venture funding machine continues uninterrupted. That bet is not obviously bad—but it is a bet, and it should be underwritten explicitly.

The Microsoft Shareholder Lawsuit: Misreading the Signal

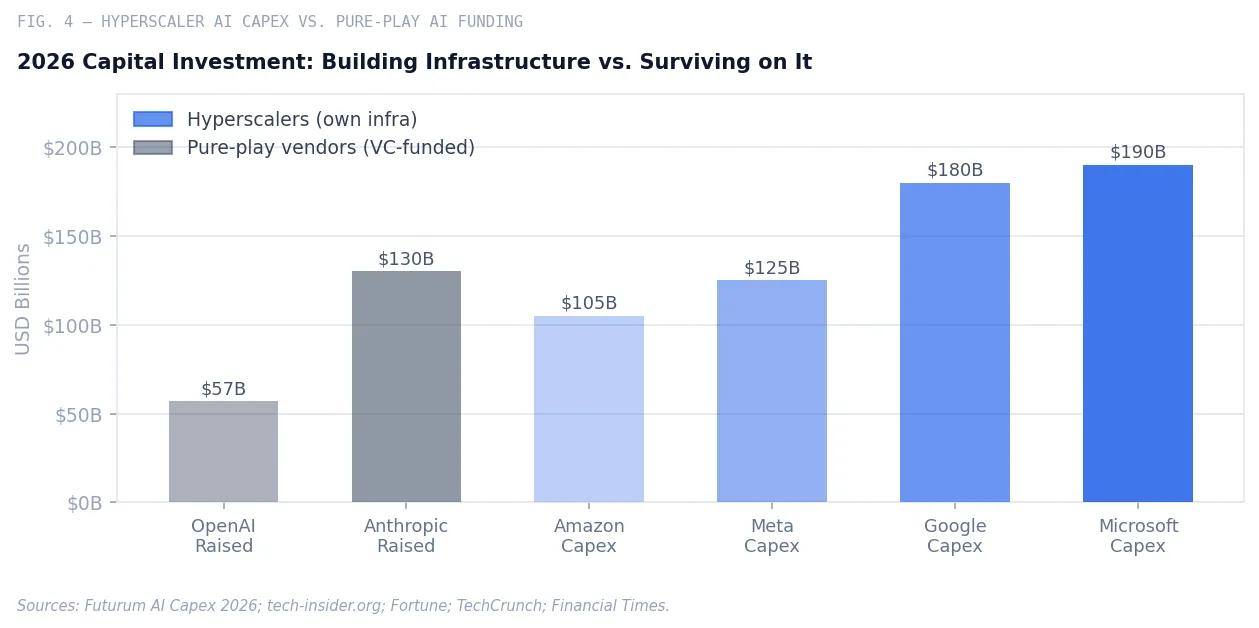

In January 2026, Microsoft reported its Q2 FY2026 earnings. Azure’s revenue growth decelerated one percentage point—from 40 percent the prior quarter to 39 percent. Capital expenditures came in at $37.5 billion for the quarter, a 66 percent year-over-year increase that exceeded every analyst estimate. Microsoft attributed the deceleration to capacity constraints driven by AI infrastructure investment. The market reacted violently: the stock fell 10 percent on January 29, erasing approximately $357 billion in market capitalization in a single session.12

A class-action lawsuit followed. Filed by the City of St. Clair Shores Police and Fire Retirement System (Michigan) in Seattle federal court, and joined by firms including Levi & Korsinsky, Robbins Geller Rudman & Dowd, and Bronstein, Gewirtz & Grossman, the complaint alleges Microsoft made materially false statements about Copilot adoption while concealing capacity limitations and the scale of required infrastructure investment.13 The lead plaintiff deadline is August 11, 2026.

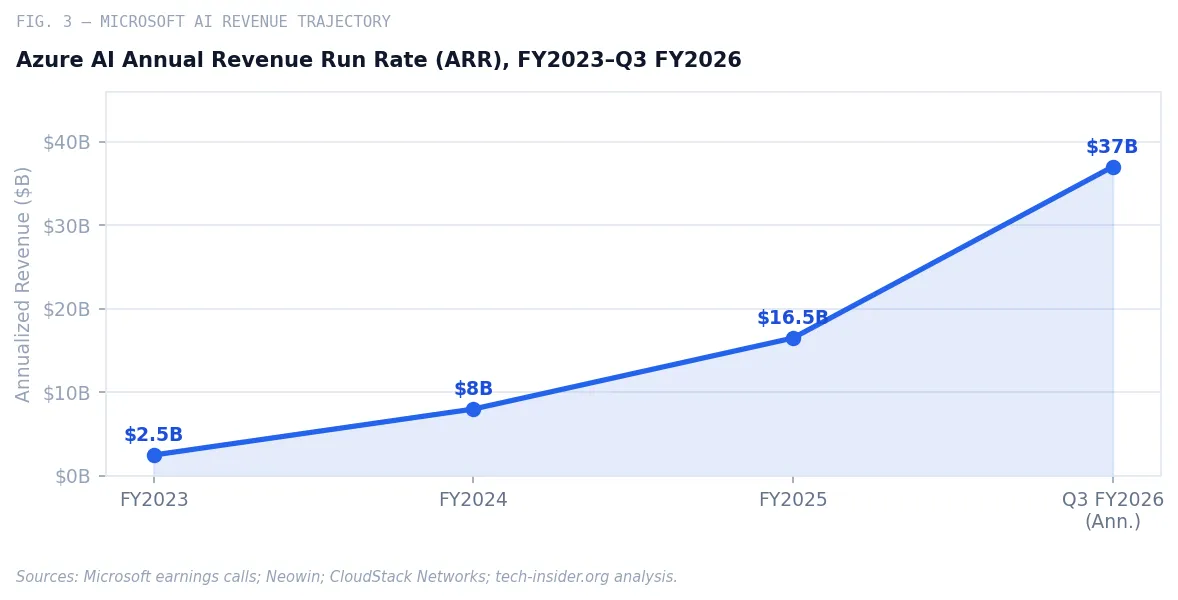

The lawsuit reflects a comprehensible frustration—shareholders who purchased between May 1, 2025 and January 28, 2026 at prices above $550 experienced concentrated losses.14 But the theory of liability is contestable on financial merits: the capex program that alarmed investors generated an Azure AI annual run rate of $37 billion in Q3 FY2026, up 123 percent year-over-year.15

Microsoft is tracking toward $120 billion or more in calendar 2026 capex, with CEO Satya Nadella raising the full-year figure to $190 billion.16 The company has an unfulfilled Azure backlog of $80 billion, constrained not by demand but by power availability.17 Commercial bookings surged 230 percent year-over-year in Q2 FY2026, with Azure’s Remaining Performance Obligations at $625 billion.18

These are not the metrics of a company concealing an AI monetization failure. They are the metrics of a company investing ahead of demand at a scale that temporarily compressed visible margin. Whether the disclosure argument in the lawsuit survives judicial scrutiny is a matter for the Western District of Washington. The underlying investment thesis is not meaningfully weakened by its existence.

Usage-Based Billing: Honesty as a Competitive Advantage

On June 1, 2026, Microsoft transitioned all GitHub Copilot plans to usage-based billing. The mechanism is straightforward: every plan now includes a monthly allotment of GitHub AI Credits (1 credit = $0.01), and usage is calculated based on token consumption—input, output, and cached tokens—at the published API rate for each model. Base plan prices are unchanged: Pro at $10/month, Business at $19/user/month, Enterprise at $39/user/month, each including a credit allotment equal to the plan price.19

| Plan | Monthly Price | Included AI Credits | Additional Credits | Billing Basis |

|---|---|---|---|---|

| Copilot Pro | $10 / user | 1,000 credits | Pay-as-you-go | Token consumption |

| Copilot Pro+ | $39 / user | 3,900 credits | Pay-as-you-go | Token consumption |

| Copilot Business | $19 / user | 1,900 credits | Pay-as-you-go | Token consumption |

| Copilot Enterprise | $39 / user | 3,900 credits | Pay-as-you-go | Token consumption |

Mario Rodriguez, VP of GitHub, explained the rationale directly in the April 27 announcement: “GitHub has absorbed much of the escalating inference cost behind that usage, but the current premium request model is no longer sustainable.”20 This is a remarkable public statement. It is, in essence, Microsoft acknowledging what much of the industry has refused to say: that subsidizing inference at flat-rate pricing is not a durable business model as agentic workloads—which involve long, multi-step reasoning sessions consuming orders of magnitude more compute than a chat prompt—become the dominant usage pattern.

“Copilot is not the same product it was a year ago. It has evolved from an in-editor assistant into an agentic platform capable of running long, multi-step coding sessions, using the latest models, and iterating across entire repositories.”

— Mario Rodriguez, VP of GitHub, April 27, 2026

Usage-based billing is not, in the first instance, a revenue maximization move. It is a signal of financial honesty. It corrects the market distortion created when heavy compute usage and light compute usage are priced identically. And it positions Microsoft to sustain the service quality and model currency that enterprise customers require over multi-year contract terms—something a company with deeply negative operating margins and a dependency on continued venture funding cannot guarantee.

The UBB Principle UBB aligns price to value consumed. For the median enterprise developer with typical usage patterns, the included credit pool covers most day-to-day work. For the heavy user running agentic sessions on frontier models, usage scales with actual compute demand. Neither party is cross-subsidizing the other—and the vendor’s economics do not depend on continued investor subsidy.

Why Microsoft Is the Structurally Superior Enterprise AI Investment

The enterprise AI decision is not, ultimately, a model quality decision—though Microsoft’s access to OpenAI’s frontier models through Azure OpenAI Service, combined with models from Meta, Mistral, and others, makes the access argument strong. The enterprise AI decision is a durability decision: which platform will exist, at current quality and pricing levels, across the 24-to-60-month planning horizon of an enterprise software commitment?

Microsoft’s financial position is structurally different from every pure-play AI vendor in the market. It is a $3 trillion market-capitalization company with $75 billion in annual Azure revenue (FY2025), approaching a $100 billion Azure run rate in 2026.22 Its AI business—Azure AI services, Copilot across Microsoft 365 and GitHub, and OpenAI-related infrastructure—is generating $37 billion in annualized revenue with 123 percent year-over-year growth.23 It is committing $190 billion in calendar 2026 capex from operating cash flows and existing capital markets access—not from venture rounds dependent on future liquidity events.24

The distinction matters because it changes the risk profile of the enterprise relationship entirely. Consider the alternatives:

| Dimension | Microsoft (Azure / GHCP / M365) | Pure-Play AI Vendors |

|---|---|---|

| Funding source | Operating cash flow + capital markets | Venture capital; dependent on future rounds |

| Profitability status | Profitable; AI as a growth segment | Deeply unprofitable; profitability 2027–2030+ |

| Inference pricing model | Usage-based; cost-aligned | Flat-rate or premium request; investor-subsidized |

| Infrastructure ownership | Owns datacenters, networking, silicon (Maia) | Rents compute from hyperscalers |

| Model breadth | OpenAI, Llama, Mistral, Phi, and others via Azure | Single-vendor or narrow ecosystem |

| Regulatory continuity risk | Low; established enterprise contract posture | Higher; exit, acquisition, or pricing disruption risk |

| Interoperability | Native integration across M365, GitHub, Azure | API-level integration; no platform depth |

The token economics argument is important. Microsoft’s UBB model—1 AI Credit = $0.01, aligned with Azure’s published API rates—creates a direct mapping between what an enterprise pays and what it consumes. An enterprise can model AI spend as a function of developer hours, codebase size, and agentic task complexity. That is a real budget line, not a flat fee obscuring unlimited variable cost exposure.

By contrast, subsidized flat-rate inference from a venture-backed vendor introduces a category of discontinuity risk that rarely appears in procurement frameworks: the risk that the vendor’s economics change before your contract ends. This materializes as sudden price increases when the next funding round demands improved unit economics, degraded model quality when inference costs must be cut, or service discontinuity in consolidation scenarios.

How to Leverage Microsoft’s AI Investment

For enterprise technology leaders, the practical implication is a framework rather than a vendor directive. The question is not “which model performs best on today’s benchmark”—model performance is converging rapidly. The question is: which platform gives you the highest confidence of cost predictability, service continuity, and economic alignment over a three-to-five-year horizon?

Several structural advantages compound for Microsoft customers. First, the MACC (Microsoft Azure Consumption Commitment) mechanism allows enterprises to apply existing Azure spend commitments against GitHub Copilot and other AI workloads, making incremental AI investment a draw-down against already-committed budget. Second, the UBB architecture creates a natural optimization loop: as developers instrument agentic workflows, usage telemetry becomes a first-order input to engineering productivity ROI calculations. Third, the breadth of the Microsoft AI ecosystem—Copilot in M365, GitHub Copilot for developers, Azure OpenAI Service for custom deployments, and Copilot Studio for low-code agent development—means AI productivity gains compound across the organization rather than accumulating in a single workflow silo.

The Hugging Face S3 bill was a meme. But the economics it surfaced are directional. Infrastructure costs for frontier AI are large, growing, and structurally unavoidable. The companies that have built durable infrastructure and designed pricing that reflects actual cost will be standing at the end of the enterprise planning horizon. The enterprises that anchored their AI strategy to subsidized pricing from venture-backed vendors will be renegotiating under very different market conditions.

Usage-based billing is not a punishment. It is the honest version of the deal. And in a market full of funny money, honesty is a durable competitive advantage.

References

- Julien Chaumond (@julien_c), post on X, June 16, 2026. Chart shows Hub storage rising from approximately 400 PB to approximately 1,200 PB following the Mistral upload—an 800 PB increase. Reported via Digg Tech, June 16, 2026.

- AWS S3 standard storage list pricing: approximately $23/TB/month (us-east-1). Amazon Web Services Pricing, accessed June 2026.

- MarketWise, “OpenAI’s Losses Surge to $21 Billion,” citing Financial Times analysis of leaked documents, June 2026.

- MarketWise, citing Q1 2026 OpenAI operating results: $5.7B revenue, negative 122% operating margin.

- Fortune / Wall Street Journal, “OpenAI Cash Burn Rate Annual Losses 2028,” November 2025; OpenAI internal investor documents.

- Software Thug, “The AI Money Pit: How Much Are OpenAI, Anthropic, and xAI Actually Losing?” February 2026.

- Ibid.; also European Business Magazine, “Sam Altman’s OpenAI Is Burning Billions,” March 2026.

- The Global Statistics, “Anthropic IPO Statistics 2026,” June 2026; Futurum, “Anthropic Files for IPO,” June 2026.

- TechCrunch, “Anthropic Raises $65 Billion, Nears $1T Valuation,” May 28, 2026; SmartAsset, “Anthropic IPO,” June 2026.

- Carta, “VC Fund Performance: Q1 2026,” accessed June 2026.

- iExchange / Crunchbase analysis cited in “The 2026 VC Playbook,” March 2026.

- Neowin, “Microsoft Faces Shareholder Lawsuit Over Masking AI Costs,” June 2026; PYMNTS, June 2026.

- Business Wire / Levi & Korsinsky, June 2026; Robbins Geller Rudman & Dowd, class action filing; Bronstein, Gewirtz & Grossman announcement.

- Live Index, “Shareholders’ Lawsuit Against Microsoft Over Expenditures,” June 2026.

- CloudStack Networks, “Microsoft Commits to Doubling AI Infrastructure,” May 2026.

- Fortune, “Microsoft, Meta, and Google Just Announced Billions More in AI Spending,” April 30, 2026.

- Futurum, “AI Capex 2026: The $690B Infrastructure Sprint,” February 2026.

- Tech-Insider, “Microsoft AI Spending 2026: $150B Capex Analysis,” June 2026.

- GitHub Blog (Mario Rodriguez), “GitHub Copilot Is Moving to Usage-Based Billing,” April 27, 2026; Schneider IT Management analysis, June 2026.

- GitHub Blog, April 27, 2026, ibid.

- InfoWorld, “GitHub Shifts Copilot to Usage-Based Billing,” April 28, 2026.

- Tech-Insider, “Microsoft AI Spending 2026,” citing Azure revenue milestones.

- CloudStack Networks, May 2026, citing Q3 FY2026 earnings.

- Fortune, April 30, 2026, citing Amy Hood Q3 FY2026 guidance.