The Signal

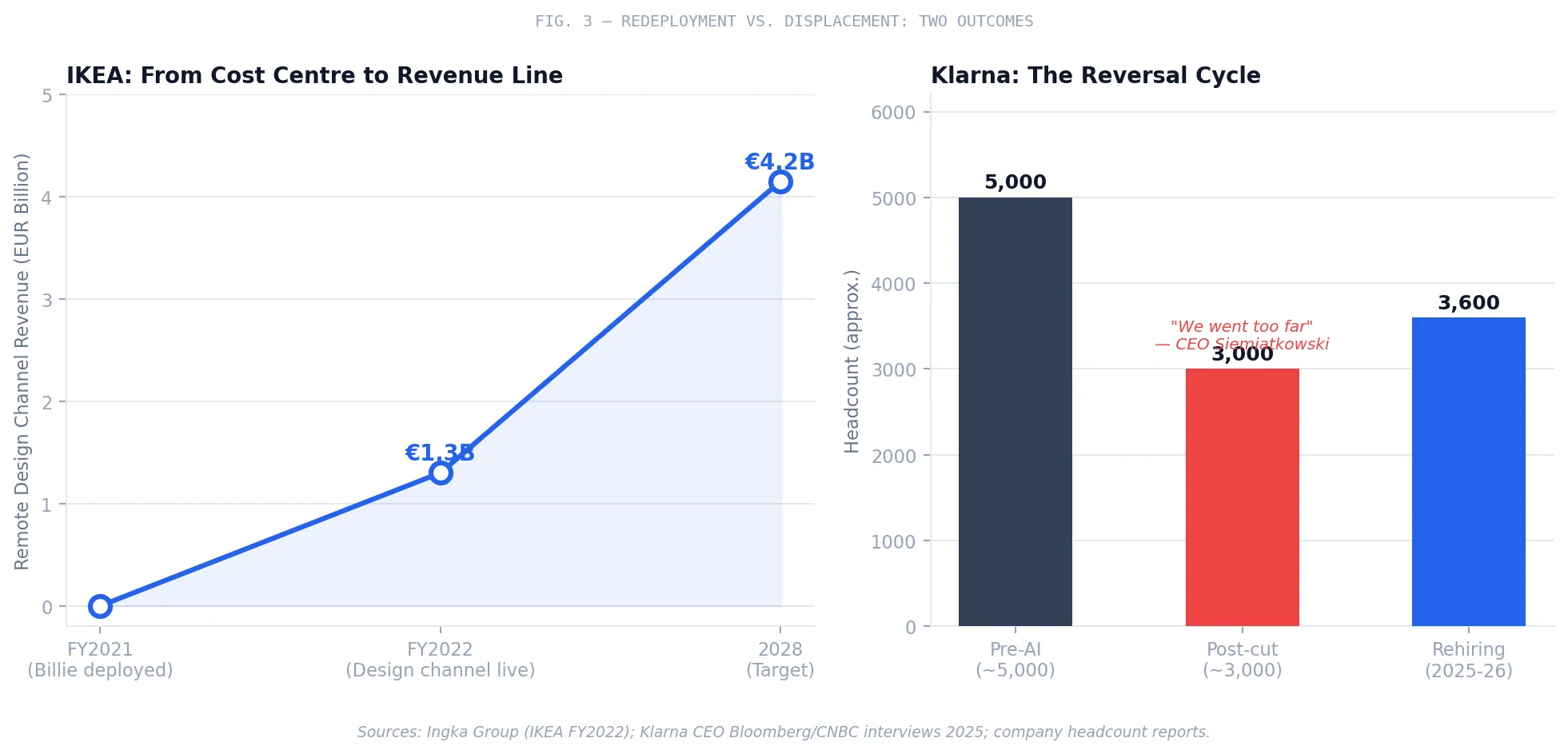

In 2021, IKEA’s customer service operation faced a familiar pressure: inbound contact volume was climbing, cost-per-interaction was a persistent drag on margins, and a growing share of queries were transactional enough to automate. The company deployed an AI chatbot named Billie, which quickly absorbed 47% of all customer inquiries—3.2 million interactions annually resolved without human intervention, yielding nearly €13 million in operational savings.1

The decision that followed is what sets the IKEA story apart from the default AI playbook. Instead of issuing redundancy notices to the 8,500 call-center employees whose roles Billie had partially displaced, Ingka Group—the largest of IKEA’s twelve franchise operators—asked a different question: What is the chatbot unable to do?

The answer was design. Customers wanted to know how the Friheten sofa would fit against the north wall of a 14-by-12 room. They wanted someone to tell them whether the BILLY bookcase in birch veneer would work alongside existing oak furniture. They wanted judgment, taste, and spatial reasoning—the human things. IKEA built a service around that latent demand. Workers were retrained in room planning, digital sales, and design consultation, then deployed into a paid advisory model priced at £25 for a 45-to-60-minute video session in the UK, scaling to £125 for a full workspace design package with a floor plan and 3D renders.

Opening Signal By the end of fiscal year 2022, IKEA’s remote interior design channel generated €1.3 billion in revenue—approximately $1.4 billion—representing 3.3% of Ingka Group’s total sales. The company has set a target of growing that channel to 10% of total revenue by 2028.2

A cost center became a revenue line. The customer service function, historically a liability measured in cost-per-contact, now generates more than a billion euros annually in a business that did not exist before the automation decision.

What IKEA demonstrated is not that AI is benign. It is that the returns from AI are captured not by the automation itself, but by what the organization does with the human capacity that automation frees.

The Structural Problem

The IKEA outcome is not the industry norm. It is the exception—and the contrast between how IKEA handled its AI deployment and how most enterprises are handling theirs is the structural problem that every VP and Director of Engineering, every line-of-business leader with a headcount budget, must now confront.

In May 2026, Meta reduced its global workforce by approximately 8,000 employees—10% of its total headcount—while simultaneously projecting capital expenditures of $115 billion to $135 billion for the year, driven by AI infrastructure investment.3 The framing in the internal memo, confirmed by NPR and other outlets, was efficiency: the cuts would “allow us to offset the other investments we’re making.”4 The employees were not redeployed. They were displaced.

Meta is not unique. Amazon announced layoffs of approximately 16,000 workers as part of an AI-linked restructuring. Block eliminated roughly 4,000 positions. Salesforce attributed approximately 1,000 cuts to automation. The pattern is consistent: enterprises announce AI investment, then announce headcount reduction as the corresponding efficiency story they tell to capital markets.5

The problem is not that these companies are adopting AI. The problem is the underlying assumption driving the workforce decision—that the value of AI is captured by reducing the number of people. The data says that assumption is wrong.

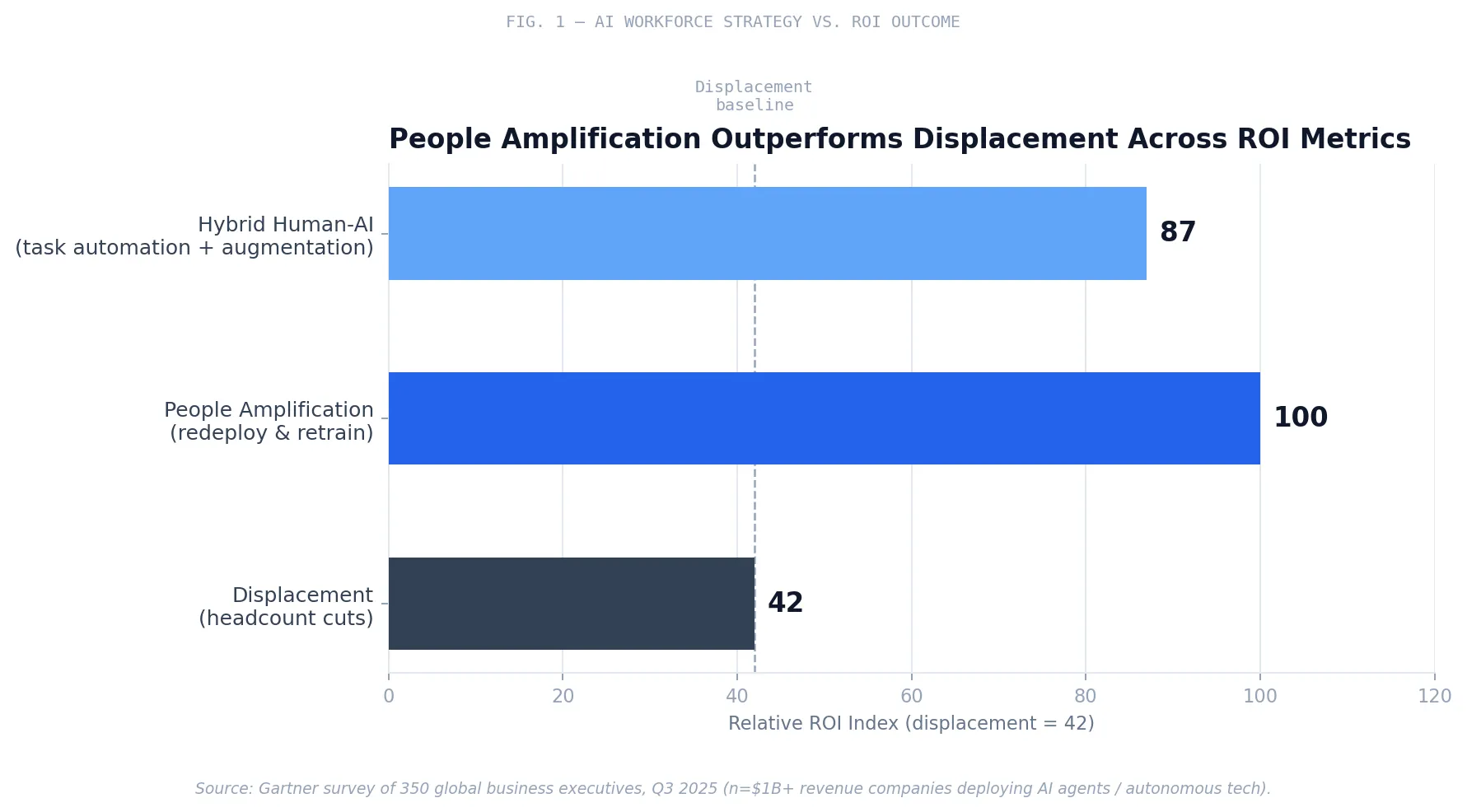

In a study released in May 2026, Gartner surveyed 350 global business executives at companies with at least $1 billion in annual revenue, all of them already piloting or deploying autonomous business capabilities including AI agents and intelligent automation. The headline finding was unambiguous: approximately 80% of those organizations reported workforce reductions tied to their AI initiatives—some by as much as 20%. Workforce reduction rates were nearly equal among organizations reporting higher ROI and those experiencing modest gains or negative outcomes. There was no statistically meaningful correlation between headcount cuts and improved financial performance from AI deployment.

“Many CEOs turn to layoffs to demonstrate quick AI returns; however, this disposition is misplaced. Workforce reductions may create budget room, but they do not create return.”

— Helen Poitevin, Distinguished VP Analyst, Gartner, May 2026

The companies that reported the strongest ROI were those using AI for what Gartner calls “people amplification”—deploying the technology to make workers more capable rather than to make workers unnecessary.6

The Mechanics

Understanding why displacement underperforms requires understanding what AI actually automates versus what it cannot.

BCG’s analysis of approximately 165 million U.S. jobs across 1,500 distinct roles, published in April 2026, offers the most granular current picture. Its finding: between 50% and 55% of U.S. jobs will be meaningfully reshaped by AI over the next two to three years. Critically, “reshaped” is not a synonym for “eliminated.” BCG distinguishes between roles that AI augments, roles it rebalances toward higher-value tasks, and roles where it substitutes for specific functions. Only 10% to 15% of jobs are projected to be fully displaced over a five-year horizon—and the firm explicitly warns that companies cutting their workforce beyond AI’s actual ability to replace it “will see productivity drop, institutional knowledge disappear, and critical talent walk away.”7

The most instructive counterexample is Klarna. The Swedish fintech made global headlines in 2023 when CEO Sebastian Siemiatkowski announced that an OpenAI-powered chatbot was conducting the equivalent work of 700 customer service agents. The company reduced its workforce from approximately 5,000 to roughly 3,000. The efficiency story appeared to work—until the quality data arrived. By early 2025, customer satisfaction scores had deteriorated materially on complex interaction types. Repeat contact rates climbed. Negative reviews referencing poor service quality became a pattern. Siemiatkowski acknowledged publicly that the company had “focused too much on efficiency and cost” and that “the result was lower quality.” Klarna began rehiring customer service agents.8

IBM followed a parallel arc. In 2023, the company replaced much of its HR division with an AI-powered system called AskHR, reducing back-office headcount by approximately 8,000 roles. When the AI proved unable to handle tasks requiring empathy or subjective judgment—which turned out to be a substantial share of what the HR function actually does—IBM reversed course and began rehiring. CEO Arvind Krishna subsequently noted that despite widespread AI adoption, IBM’s total employment had actually increased, because AI-generated efficiency freed investment that the company redirected into other areas.9

The pattern is consistent enough to have earned a name. Analyst firm Robert Half reports that approximately 29% of companies that cut staff due to AI integration have already reopened and rehired for those exact positions. Gartner projected, in February 2026, that half of all AI-driven layoffs will reverse by 2027.10

The Mechanics AI automates tasks. It does not replace the organizational capability to do complex, judgment-intensive, relationship-dependent work. Companies that treat these as equivalent are making permanent workforce decisions based on a temporary, incomplete view of what AI can actually substitute.

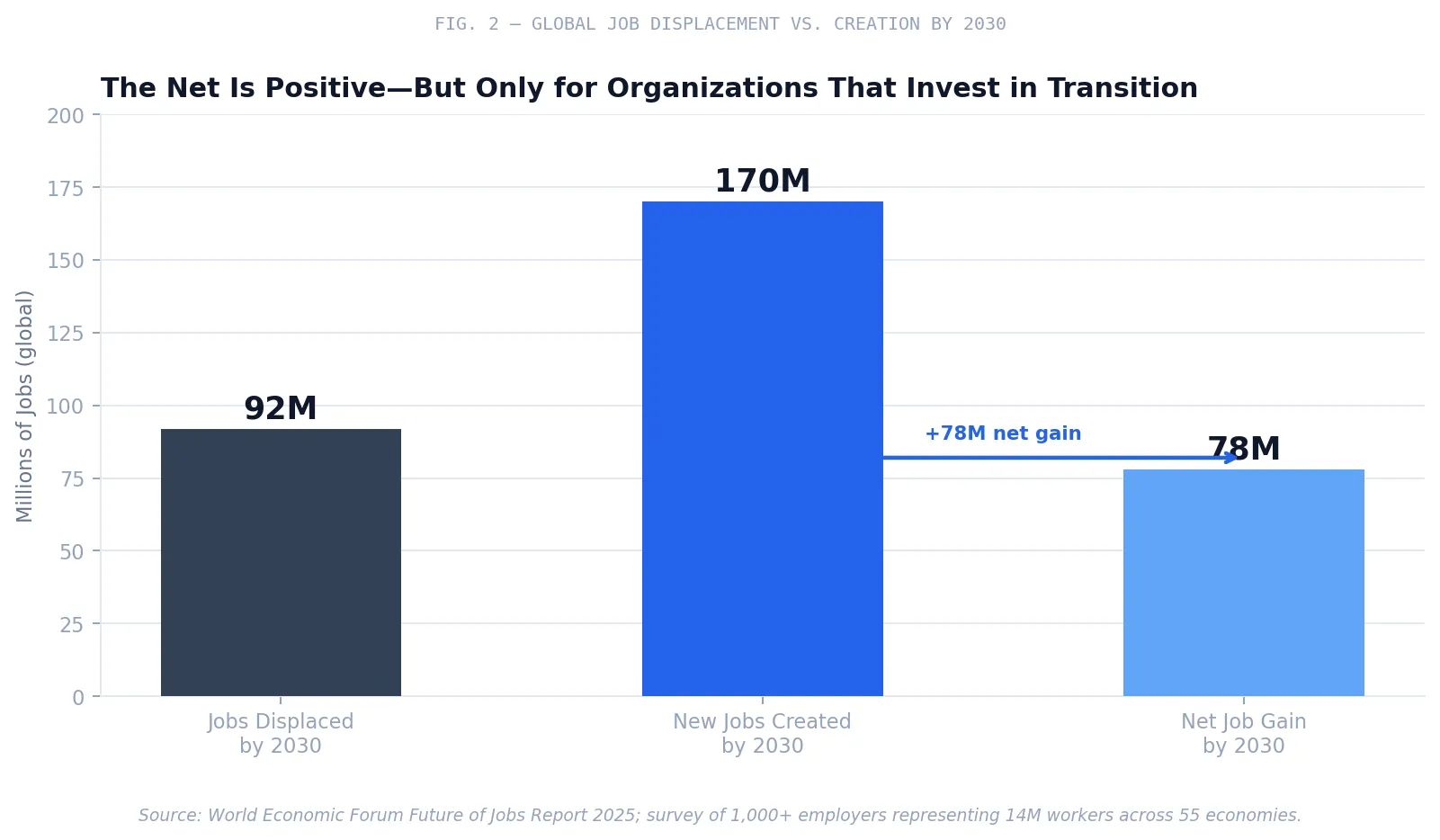

The WEF Future of Jobs Report 2025, drawing on surveys of more than 1,000 employers representing 14 million workers across 55 economies, projects that by 2030, 170 million new roles will be created globally while 92 million are displaced—a net positive of 78 million jobs.11

The math of net job creation is real. But the math assumes transition. It assumes that workers displaced from one role can, with investment and time, move into another. Companies that eliminate people without building that pathway are not participating in the net positive. They are absorbing only the displacement side of the equation and passing the transition problem to their workers, their communities, and eventually their own talent pipelines.

The Enterprise Implication

The talent pipeline argument deserves particular attention from engineering and line-of-business leaders, because it is the one most likely to be understated in a headcount conversation.

Professor Dilan Eren of Ivey Business School has described the elimination of junior roles as an “exponentially bad move” that threatens the internal talent pipeline. The observation is specific: organizations that cut entry-level positions to achieve near-term efficiency savings are eliminating the mechanism by which mid-level and senior roles are developed. Senior engineers, technical leads, and solution architects do not appear fully-formed. They develop through years of structured exposure to lower-complexity problems, mentorship relationships, and incremental responsibility accumulation. Cutting the junior layer does not accelerate that development for the remaining population; it severs the pipeline that feeds it.12

Separate research published through arXiv in early 2026 documented what its authors call the “missing junior loop”: a 16% relative decline in employment for workers aged 22 to 25 in AI-exposed occupations, concentrated in roles where AI is used as a substitute for execution rather than as a complement to accumulated experience. The study found that occupations where AI augments human judgment remained stable or grew. Those where AI substituted for it shrank—and the developmental function those junior roles serve within organizations shrank with them.13

The implication for a VP of Engineering is direct: an AI-augmented senior team that has eliminated its junior layer is borrowing against the future. The productivity gains are real and immediate. The cost—a depleted pipeline for the next generation of technical leadership—is deferred and diffuse enough to be invisible until it is not.

| Strategy | Near-Term Cost Signal | ROI Outcome | Talent Pipeline Effect | Reversibility |

|---|---|---|---|---|

| Role Displacement (cut headcount) | Immediate savings, budget freed | No correlation with improved ROI (Gartner) | Junior pipeline disrupted; institutional knowledge lost | Low—rehiring is expensive; 29% already reversing |

| Role Reassignment (retrain, redeploy) | Upfront training investment | Highest ROI cohort in Gartner study | Skills updated in place; institutional knowledge preserved | High—role redesign is iterative and adjustable |

| Hybrid (automate tasks, augment people) | Moderate—automation savings offset by retention investment | Consistently outperforms full automation (Klarna reversal data) | Develops AI-fluent talent across experience levels | High—model can be adjusted as AI capabilities evolve |

There is also a direct financial counterargument to the displacement strategy that deserves placement in any headcount conversation: rehiring costs. The Klarna case makes this concrete. Reversing AI-driven layoffs requires recruiting, onboarding, and training new staff—an expense that is rarely modeled in the original business case for displacement. The true cost of full replacement includes the cost of unwinding it when it fails. When 55% of employers already report regretting AI-driven workforce reductions, the probability that the unwind cost needs to be modeled is not theoretical.14

Counterarguments the Data Must Address

The case for displacement rests on three arguments that deserve direct engagement.

The first is speed. Displacing workers is faster than redeploying them. Retraining takes time; an organization trying to capture AI productivity gains at competitive speed cannot afford a multi-year reskilling program. This is the strongest version of the counterargument, and it has partial merit. The IKEA retraining timeline was not a weekend workshop—it was a sustained investment in curriculum design, delivery, and role redesign. But the Gartner data reframes the question: if displacement does not improve ROI, then speed-to-displacement is speed-to-a-worse-outcome. Moving faster in the wrong direction is not a competitive advantage.

The second is structural misalignment. Some roles do not have an adjacent higher-value counterpart. The IKEA scenario worked because call-center skills—listening, explaining, managing frustration, building rapport—transfer directly into design consulting. Not every function has that adjacency. This is a real constraint, and it argues for role-by-role analysis rather than a blanket redeployment mandate. BCG’s segmentation model, which distinguishes between roles where AI augments versus substitutes, is the right analytical tool for this mapping exercise. The answer is not “redeploy everyone regardless of adjacency.” It is “do the analysis before you decide.”

The third is that the macro numbers—WEF’s 78 million net new jobs, BCG’s 50-to-55% reshaping figure—assume a functioning reskilling infrastructure that does not yet exist at most organizations. This is the most serious objection. Only 6% of organizations surveyed in a 2024 BCG study reported having begun upskilling “in a meaningful way,” despite 89% acknowledging the need. The gap between intention and execution is real. It is also an argument for starting now, not an argument for defaulting to displacement in the interim.15

The Action Framework

For an engineering leader or line-of-business VP with a headcount budget and an AI adoption mandate, the strategic path is not complicated, but it is specific.

Map before you cut. Before any headcount decision tied to AI deployment, conduct a task-level analysis of affected roles. BCG’s six-category segmentation provides a framework: which roles are being amplified, rebalanced, substituted, or diverged? The answer determines whether displacement or redeployment is the appropriate response—and for most roles, BCG’s data suggests redeployment is the answer.

Distinguish budget room from return. The Gartner finding should be a standing agenda item in any AI ROI conversation: workforce reduction creates budget room. It does not create return. The CFO who is modeling AI investment as headcount reduction offset is modeling the wrong variable. Push the conversation toward revenue per employee, output quality, and pipeline health—the metrics where people-amplification strategies produce measurable gains.

Protect the junior layer. If the organization is eliminating entry-level roles as AI absorbs entry-level tasks, it is also eliminating the developmental mechanism for its next generation of technical leaders. This is a decision that will not surface as a problem for two to three years—long after the headcount budget shows savings. Engineer the reskilling investment to flow to that layer, not just to mid-level employees who are already competent.

Use attrition, not elimination. JPMorgan’s model is instructive. The bank’s total headcount remained broadly stable at 318,512 over the past year, while internal composition shifted: operations and support roles declined 4% and 2%, respectively, through attrition, while revenue-producing and front-office support roles grew 4%. AI-driven productivity improvements—an 11% reduction in per-unit fraud costs, 10% improvement in software engineer efficiency, a 6% increase in accounts handled per operations employee—were achieved without a mass displacement event. CEO Jamie Dimon has been explicit: “We already have huge redeployment plans for our own people. We have displaced people from AI—and we offer them other jobs.”16

Action Principle Attrition-paced redeployment lets AI-driven efficiency gains accumulate without triggering the rehiring costs, institutional knowledge loss, and pipeline disruption that follow mass displacement. It is slower and requires more management discipline. It is also what the data shows works.

Model the full cycle cost. Any displacement business case that does not include the probability-weighted cost of reversal is an incomplete model. Gartner projects half of AI-driven layoffs will reverse by 2027. Robert Half finds 29% already have. Build those numbers into the analysis before the decision, not after.

Closing

The IKEA outcome is reproducible—not because every company sells furniture or because every displaced worker can become a design consultant, but because the underlying logic generalizes. Automation identifies what machines can do. The management decision is what to do with the human capacity it frees. Companies that answer that question with displacement are capturing AI’s cost reduction while discarding its amplification potential. Companies that answer it with redeployment are capturing both—and the data is increasingly clear about which approach produces the returns. Gartner forecasts that autonomous business will become a net job creator by 2028 to 2029.17 The enterprises best positioned for that shift will be the ones that invested in their people while their competitors were eliminating them.

References

-

Ingka Group Newsroom, “Billie the chatbot,” cited in Scott M. Robertson, “How IKEA Turned 8,500 Call Centre Workers Into Interior Design Advisors Using AI,” Substack, April 21, 2026; and PYMNTS, “IKEA Turned 8500 Call Agents Into Design Consultants,” May 19, 2026.

-

Ingka Group, cited in Fluent Support, “How IKEA Turned AI ‘Failures’ Into €1.3 Billion in Revenue,” April 2026; Reuters, cited in PYMNTS, May 19, 2026. Revenue figure: €1.3 billion (≈ $1.4 billion at prevailing exchange rates), FY2022. Target: 10% of total Ingka revenue by 2028.

-

Meta Platforms, Q4 2025 earnings report; Variety, “Meta Laying Off 8,000 Employees, 10% of Workforce, Amid Surge in Spending on AI,” April 23, 2026. Capex guidance: $115–$135 billion for 2026, per Meta January 2026 earnings.

-

NPR, “Meta slashes 8,000 jobs as it pivots towards AI,” May 20, 2026. Internal memo quoted by company spokesperson Erica Sackin.

-

Axios, “Meta to lay off 8000 as part of AI efficiency push,” April 23, 2026; CNBC, “20,000 job cuts at Meta, Microsoft raise concern that AI-driven labor crisis is here,” April 24, 2026.

-

Gartner, “Gartner Says Autonomous Business and AI Layoffs May Create Budget Room, but Do Not Deliver Returns,” press release, May 5, 2026. Survey: 350 global business executives, Q3 2025, minimum $1 billion annual revenue.

-

Boston Consulting Group, “AI Will Reshape More Jobs Than It Replaces,” April 2026. Analysis covers approximately 165 million U.S. jobs across 1,500 distinct roles using Revelio Labs data.

-

Klarna CEO Sebastian Siemiatkowski, Bloomberg interview, May 2025; CX Dive, “Klarna again recruits humans for customer service after AI push,” September 2025; Digital Applied, “Klarna Reverses AI Layoffs: Why Replacing 700 Failed,” March 2026.

-

IBM CEO Arvind Krishna, Wall Street Journal interview, cited in ACS Information Age, “Companies backtrack after going all in on AI,” May 2025.

-

Gartner, press release, February 3, 2026. Kathy Ross, Senior Director Analyst, Gartner Customer Service & Support practice. Robert Half, talent consulting data cited in flowbots.ai, “15 Companies That Replaced Workers with AI—And What Happened Next,” March 2026.

-

World Economic Forum, Future of Jobs Report 2025, January 8, 2025. Survey: 1,000+ employers, 14 million workers, 55 economies. Net figure: 170 million new roles created against 92 million displaced, yielding net positive of 78 million jobs by 2030.

-

Professor Dilan Eren, Ivey Business School, quoted in AIM Multiple, “Top 20+ Predictions from Experts on AI Job Loss,” 2026.

-

“Some Simple Economics of AGI,” arXiv, 2026 (arXiv:2602.20946). Documents 16% relative employment decline for workers aged 22–25 in AI-exposed occupations with substitutive AI use, versus stable or growing employment in augmentative AI use contexts.

-

Forrester, Predictions 2026, cited in Metaintro, “Half of AI-Driven Layoffs Will Reverse by 2027, Gartner Says,” February 3, 2026. Forrester finding: 55% of employers who restructured for AI now regret the decision.

-

BCG, cited in IBM Think, “AI Upskilling Strategy,” November 2025. Survey: 89% of respondents said workforce needs improved AI skills; 6% had begun upskilling in “a meaningful way.”

-

JPMorgan Chase CEO Jamie Dimon, investor meeting remarks, February 24, 2026, reported by CNBC, “Jamie Dimon says AI is already reshaping JPMorgan Chase’s workforce as bank plans ‘huge redeployment.’” Operational metrics: JPMorgan investor presentation, February 2026.

-

Gartner, May 5, 2026 press release. Forecast: autonomous business will become a net job creator by 2028–2029. AI agent software spending projected at $206.5 billion in 2026 and $376.3 billion in 2027.